Project finance explained: structure, risks, and success factors

- Janet

- Mar 31

- 8 min read

Most corporate decision-makers assume project finance is simply a large business loan. It is not. Project finance uses specialized structures to isolate projects from company balance sheets, meaning lenders rely on the project’s own cash flow rather than the sponsor’s corporate assets. This distinction changes everything: how risk is allocated, how capital is structured, and how large-scale ventures in Africa and Dubai get funded. In this article, we break down the core mechanics, key financial benchmarks, risk management principles, and real-world examples so you can evaluate whether project finance is the right tool for your next initiative.

Table of Contents

Key Takeaways

Point | Details |

Project finance structure | Project finance uses SPVs and non-recourse debt so lenders rely on the project’s cash flow. |

Risk and contract management | Risks are meticulously allocated through contracts, protecting sponsors and lenders. |

Critical benchmarks | Success depends on hitting key ratios like DSCR of 1.25+, LLCR 1.3+, and LTV under 60%. |

Real-world application | Major African and Dubai projects demonstrate how strong contracts and risk allocation drive results. |

Defining project finance: Structure and key concepts

At its foundation, project finance is the funding of long-term projects using a non-recourse or limited recourse structure. Non-recourse means lenders cannot pursue the sponsor’s broader corporate assets if the project fails. Limited recourse means sponsors carry some liability, but only within defined boundaries. Both models shift the primary repayment obligation to the project itself.

The vehicle that makes this possible is the Special Purpose Vehicle (SPV). An SPV is a legally separate entity created solely to own and operate the project. It ring-fences the project’s assets, liabilities, and cash flows from the parent company. This isolation is what makes project finance mechanics fundamentally different from a standard corporate loan.

Here is a quick overview of the core components:

SPV: Legally separate entity that owns the project

Debt: Typically 70 to 90% of total project cost, sourced from banks or development finance institutions

Equity: Contributed by project sponsors, usually 10 to 30%

Cash flow: The sole source of debt repayment and investor returns

Collateral: Project assets, contracts, and revenue streams, not corporate balance sheets

Component | Role in project finance |

SPV | Isolates project risk from sponsor |

Senior debt | Primary funding source, first repayment priority |

Equity | Sponsor’s skin in the game |

Off-take agreements | Guarantee future revenue streams |

Security package | Protects lenders via project asset pledges |

“The SPV structure is not just a legal formality. It is the mechanism that makes large-scale, high-risk projects financeable by distributing exposure across multiple parties rather than concentrating it on one sponsor.”

Understanding this structure is essential before engaging any lender or financial advisor. If you are exploring how this fits within your broader corporate finance structure, the SPV model offers a powerful way to pursue growth without overextending your balance sheet.

How project finance actually works: The mechanics

With the core features outlined, it is time to unpack the day-to-day logic and process behind a typical project finance arrangement. Project finance involves SPV creation and risk allocation via contracts such as EPC and off-take agreements. Each contract serves a specific protective function.

Here is a step-by-step breakdown of how a deal comes together:

Project identification: Sponsors identify a viable project with predictable long-term cash flows, such as a power plant, toll road, or industrial facility.

Feasibility and structuring: Financial advisors assess technical, commercial, and legal viability. Capital structure is designed, balancing debt and equity.

SPV establishment: A new legal entity is incorporated to own the project exclusively.

Contract execution: Key agreements are signed, including the EPC (Engineering, Procurement, and Construction) contract, the O&M (Operations and Maintenance) agreement, and off-take agreements with buyers.

Risk allocation: Each risk allocation contract assigns specific risks to the party best positioned to manage them. Construction risk goes to the EPC contractor. Revenue risk is mitigated by off-take agreements.

Financial close: Lenders commit funds once all conditions are satisfied and documentation is complete.

Construction and operations: The project is built and begins generating cash flow, which services the debt.

Lenders protect themselves through step-in rights, which allow them to take operational control of the SPV if the project underperforms or defaults. This is a critical safeguard that makes high-leverage financing possible.

Pro Tip: Invest heavily in business documentation essentials before approaching lenders. Incomplete or inconsistent documentation is the single most common reason project finance deals stall at due diligence. A well-prepared information memorandum signals credibility and accelerates financial close.

For projects with cross-border components, understanding trade finance structures alongside project finance can open additional funding channels and reduce overall capital costs.

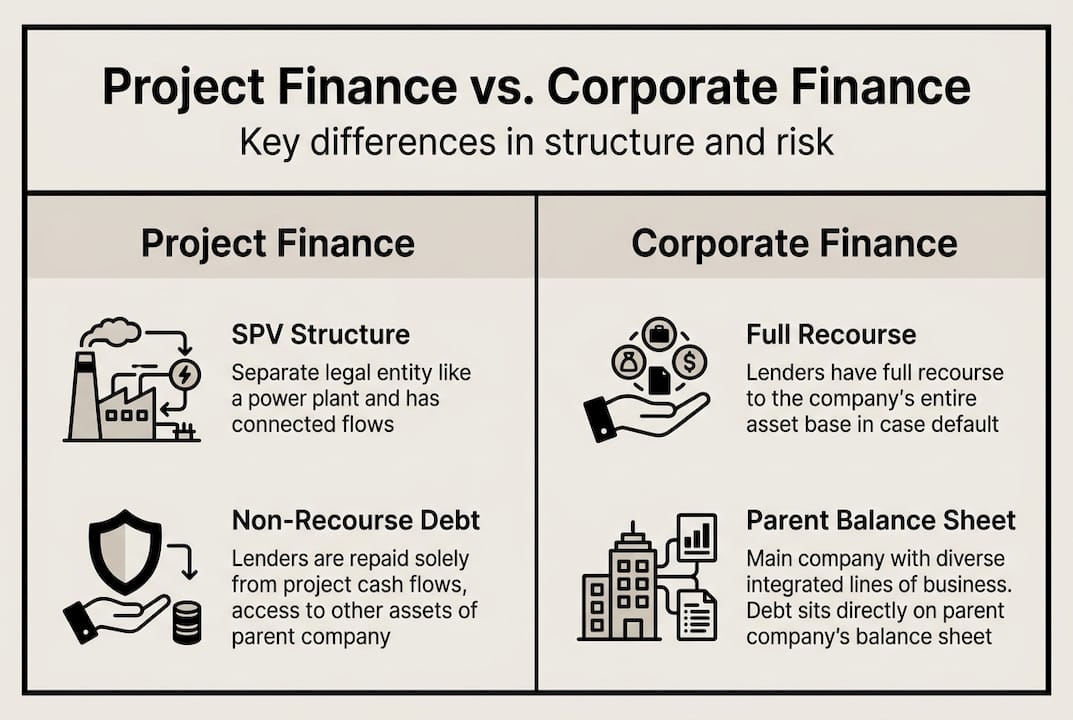

Project finance vs. corporate finance: Key differences

Understanding the mechanics begs another question: why not just use regular corporate finance? The answer lies in risk exposure and balance sheet impact. Project finance uses SPVs and non-recourse structures while corporate finance relies on company balance sheets.

Feature | Project finance | Corporate finance |

Recourse | Non-recourse or limited | Full recourse to company |

Balance sheet impact | Off-balance sheet via SPV | On-balance sheet |

Repayment source | Project cash flows only | Company revenues and assets |

Risk allocation | Distributed via contracts | Concentrated on sponsor |

Typical use case | Infrastructure, energy, resources | Working capital, acquisitions |

Leverage ratio | 70 to 90% debt | Typically 40 to 60% debt |

Corporate finance is faster and simpler. It suits short-term capital needs, acquisitions, or operational funding where the company’s creditworthiness is strong. Project finance suits long-duration, capital-intensive ventures where the project’s own economics justify the investment.

In Africa and Dubai, this distinction is especially relevant. A Kenyan developer building a 300 MW wind farm cannot realistically put that risk on a corporate balance sheet. An SPV-based project finance structure allows the developer to attract international lenders, development finance institutions, and equity partners without jeopardizing the parent company.

For a deeper look at how these models compare in practice, our project finance articles cover regional case studies and structuring strategies. You can also review our corporate finance overview to understand when each approach delivers the most value.

Risk management and benchmarks in project finance

Comparing the models surfaces another concern: risk. Here is how professional project financiers face and allocate it. Risks include construction delays, demand shortfalls, operational hazards, and financial volatility, with risk allocation achieved through contracts and lender step-in rights.

The four primary risk categories are:

Construction risk: Cost overruns, delays, or contractor default. Managed through fixed-price EPC contracts and performance bonds.

Operational risk: Equipment failure, management inefficiency, or regulatory changes. Addressed via O&M agreements and insurance.

Market and demand risk: Revenue shortfalls due to price drops or reduced demand. Mitigated by long-term off-take agreements.

Financial risk: Interest rate movements, currency fluctuations, and refinancing exposure. Managed through hedging instruments and fixed-rate debt structures.

Beyond risk allocation, lenders evaluate every project against specific financial benchmarks. Standard project finance ratios include a DSCR minimum of 1.25 to 1.3x, an LLCR of 1.3 to 1.5x, and an LTV capped at 60%.

Here is what each ratio means in practice:

DSCR (Debt Service Coverage Ratio): Measures whether the project generates enough cash to cover annual debt payments. A ratio of 1.25 means the project earns 25% more than it owes each year.

LLCR (Loan Life Coverage Ratio): Assesses whether projected cash flows over the loan’s life are sufficient to repay the debt in full.

LTV (Loan to Value): Limits the loan amount relative to the project’s appraised value, protecting lenders against asset depreciation.

“A project that cannot demonstrate a DSCR above 1.25 will struggle to attract senior debt, regardless of how strong the sponsor’s balance sheet is. Lenders fund the project, not the promise.”

Pro Tip: Do not rely on sponsor guarantees to compensate for weak project economics. Lenders in mature project finance markets prioritize risk management strategies and contractual protections over personal or corporate guarantees. Build your deal around strong benchmarks from the start. Our team can help you understand DSCR and benchmarks and structure your project to meet lender requirements. For guidance on lender protection measures, we offer targeted support at every stage.

Project finance in practice: African and Dubai success stories

The theory only matters if it delivers results. Let us look at impactful African and Dubai deals that set new benchmarks for project finance. Lake Turkana Wind, Niakhar Solar, and Ras Ghareb Wind are leading examples of how structured project finance transforms large-scale energy ambitions into operational reality.

Project | Country | Capacity | Debt/Equity split | Key lenders |

Lake Turkana Wind | Kenya | 310 MW | 75% / 25% | AfDB, EIB, DEG |

Niakhar Solar | Senegal | 60 MW | 70% / 30% | IFC, local banks |

Ras Ghareb Wind | Egypt | 262 MW | 80% / 20% | EBRD, IFC, commercial banks |

Here are the key lessons these deals teach:

SPV discipline: Each project used a dedicated SPV, keeping project liabilities separate from sponsor balance sheets.

Stakeholder alignment: Governments, developers, lenders, and off-takers were aligned through long-term power purchase agreements (PPAs), reducing revenue risk.

Robust contracts: Fixed-price EPC contracts and performance guarantees protected lenders against construction overruns.

Development finance institutions (DFIs): Participation from institutions like the African Development Bank and IFC provided credibility that attracted commercial lenders.

Dubai’s capital markets play a growing role in financing African infrastructure. The city’s position as a regional financial hub means that deals structured through Dubai-based entities can access deeper liquidity pools and more favorable terms. Our Zanzibar investment example illustrates how this cross-regional approach creates real value. You can also explore our trade finance case study and the Dubai-Africa project finance link for additional context on how these markets connect. More regional stories are available in our Africa project finance stories section.

How Maramoja Enterprises can help your next project

Ready to move from insight to action? Structuring a project finance deal requires more than financial knowledge. It demands precise documentation, credible risk allocation, and relationships with the right lenders and institutions.

At Maramoja Enterprises, our investment advisory experts guide clients through every stage of the project finance process, from feasibility assessment and SPV establishment to financial modeling and lender negotiations. We specialize in preparing bankable documentation that meets international lender standards, and we have deep experience across African markets and Dubai. Our risk management support ensures your deal is structured to satisfy DSCR, LLCR, and LTV benchmarks before you approach any lender. When you are ready to secure funding, our streamlined loan procurement service connects you with the right capital partners. Contact us today to schedule a consultation and take the next step toward financial close.

Frequently asked questions

What types of projects typically use project finance?

Project finance funds infrastructure and industrial projects via non-recourse structures. Large energy, renewable resource, transportation, and public utility projects are the most common applications.

How does project finance protect sponsors from risk?

Project finance isolates project risks through SPVs, making only project cash flows available to lenders. This means sponsors’ losses are limited to their equity contribution, not their broader corporate assets.

What financial ratios do lenders look for in project finance?

Standard project finance ratios require a DSCR above 1.25, an LLCR over 1.3, and an LTV no higher than 60%. Meeting these benchmarks is essential for achieving financial close.

Can project finance be used by businesses of any size?

Project finance is designed for long-term infrastructure, industrial, or public service projects with high capital requirements. It is best suited for large-scale ventures with predictable, contracted revenue streams rather than small or early-stage businesses.

Recommended

Comments